Financial Health for Your eCommerce Business

So you’ve got a great product, and a great website to sell it, but does your eCommerce business have the right financial processes in place to survive?

According to a recent survey by Small Business Trends, about 90% of eCommerce businesses fail in their first 4 months. Process-related issues like “running out of cash,” and/or “price and costing issues” were cited by at least a third of their respondents – circumstances that are often preventable by developing & sticking with business procedures.

These processes and procedures are often collectively referred to as “financial hygiene.” Just like our personal hygiene keeps us healthy, we need to maintain good financial habits to preserve our financial health.

- Hire a CPA When Launching Your Business

- Open Your Mail

- Maintain Accounting Controls

- Reconcile All Financial Accounts

- Anticipate Expenses

- Keep an Eye on Debt

Hire a CPA When Launching Your Business

A Certified Public Accountant (CPA) can help you set your business up correctly. If you’ve already launched, he or she can still get your bookkeeping going in the right direction before costly problems arise.

It’s true that software like Sage and Quickbooks make it easy to do your own bookkeeping. In fact, most CPAs are happy to help you learn how to work with accounting software. But failing to properly set up your chart of accounts can leave you in the dark, with a setup that’s poorly designed for your particular industry or situation.

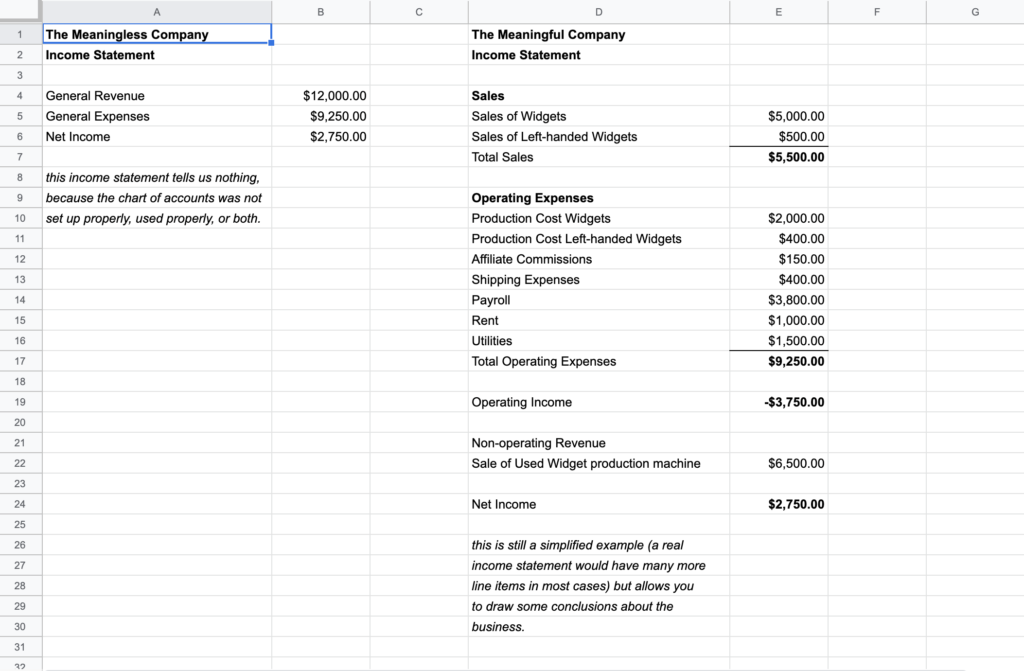

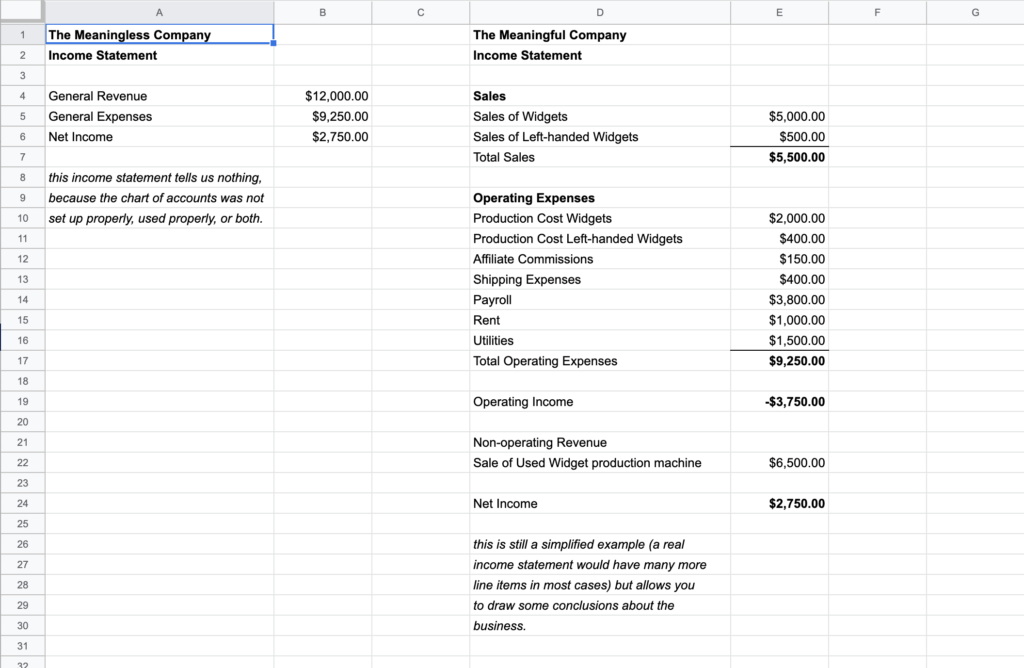

As an example, I once served on a board where the accounting software wasn’t telling us anything about our financial position. All of our revenue went into one account called “general revenue,” and all of our expenses came out of one account called “general expenses.” Sure enough, our reports were pretty meaningless.

Establishing a few accounts that captured how our funds were coming in and going out made our finances come alive.

Same bottom line, but just a few minutes spent looking at it could tell you:

- Left handed widgets are far less profitable than the regular ones (compare sales and the cost of making them)

- Even though you took in more money than you spent, you lost money selling widgets. Selling a piece of equipment masked a serious shortfall.

Proper bookkeeping throughout the year allows you and your CPA to anticipate your tax liabilities and plan ahead. It also makes the process of creating your tax return relatively simple, because your business expenses are already properly allocated to the right categories, like automotive expense, travel expenses, meals, and so on.

Without proper bookkeeping, your expenses must be figured out after the fact (if you still can). Many deductions are lost because a business owner did not keep adequate records and receipts to attest to them.

A CPA or a qualified business consultant should also help you develop realistic budgets and goals for your business, so that you can develop forecasts and know how much capital you need to launch your business.

Open Your Mail

You might be surprised how many business owners neglect to open their mail (whether electronic or postal) and take care of it. Sure, much of it will be junk, But taking care of your bank statements, government notices, and customer correspondence will keep your business on track and keep small problems from turning into bigger ones.

For example, a government notice that your sales tax payment is missing generally comes with a small penalty and interest charge – if you catch it the first time – but these costs soar if you ignore the initial notices.

Set aside a time at least once a week (preferably more often) to go through everything and process it:

- Pay bills

- Deposit checks

- Respond to customer complaints or concerns (even the difficult ones)

- Respond to vendor, bank and government notifications

You may think the advice to “deposit checks” above is unnecessary. But I was once asked to shred a number of old documents for a client, and found almost a dozen unopened envelopes with checks in them totaling over a thousand dollars – checks that were now long out of date.

If something comes in that you simply don’t understand how to handle, talk to your CPA or another trusted advisor. One of my college instructors gave my class simple advice that has always stuck with me:

“Bad news doesn’t get better with time”

Maintain Accounting Controls

As your business grows, the items mentioned above are often the first things a business owner wants to delegate. However, maintaining good accounting controls dictate that you, the business owner, personally perform certain tasks whenever possible.

If you have someone else writing your paper checks, you should still sign them. You may have someone else reconciling your bank statements, but you should still read them. The mundane task of checking the PO box has saved more than one business owner from continued fraud or theft within their organization, because they noticed an invoice or other document that didn’t make sense and tracked it down.

Reconcile All Financial Accounts

Reconciling bank and credit card statements should be performed monthly. Reconciling statements means comparing them to your records to ensure the totals are the same. Online banking and the daily transaction download to your accounting software is a good thing, but reconciling keeps your records accurate and provides a check on whether the amounts being stated are going where you believe they’re going.

For example, Quickbooks may assume that a downloaded transaction for $100 matches a transaction you’ve already entered for $100. But those amounts may just happen to match, and in fact the transaction you entered may still be outstanding.

Reconciling accounts forces you to track down all of these transactions, and is also a second chance to notice where payments have been made. For example, you may have thought you put Google AdWords on hold, but find that it’s still being charged to a credit card.

Taking inventory of your finished goods, work in progress, and raw materials periodically also helps you to keep your business records on point – and can help you discover it if things are going missing.

Anticipate Expenses

Some expenses, like ordering inventory and paying shipping bills, are predictable. Others, like payroll, taxes, and loan payments, come in at different times (weekly, bi-weekly, monthly, quarterly, or even annually).

It may be tough to keep track of how much you will owe at different times. To make it even more tricky, payroll expenses are often automatically deducted from your account, ready or not!

One solution for this is to maintain a cash flow forecast that accounts for all anticipated future expenses in the next few months. Another approach that many business owners use, especially for payroll expenses, is to maintain a separate bank account. By transferring the gross (i.e. total) amount of payroll expense to it each pay period, the business owner can effectively save up for monthly and quarterly payroll taxes as they come due.

Dedicated checking accounts are also sometimes used for significant business expenses like inventory. Depositing a portion of the money from all sales into an inventory checking account means you are always financially ready to order more inventory.

For expenses that are predictable, but that will be realized at somewhat unpredictable intervals (like the payroll and inventory examples), the additional bank accounts are preferred by many business owners because they provide a clearer picture of where they stand, without having to make calculations on the fly.

For example, if you need a new $2,000 computer in a hurry, you have $6,000 in the main bank account, and you know that your next payroll is already transferred to the payroll account, you know you’re able to buy the computer.

You’ll still need to do cash flow forecasting, but having a few dedicated checking accounts for those critical functions described above will help you stay organized, and your business should have money for your priorities.

Keep an Eye on Debt

A certain amount of debt may be inevitable in a business, especially when it’s starting up and/or growing. But unless you carefully monitor debt, your access to credit may mask serious issues with cash flow and profitability in your business. You may simply wake up one day and find that your credit cards and/or business line of credit are tapped out.

To avoid this, you should monitor your debt – check your balances at least once a month to make sure they’re heading down, not up. Keep a spreadsheet so that you see how these balances are changing over time. Creeping debt is much easier to correct before it gets completely out of hand than it will be later when you’re running out of credit and paying a lot of interest.

Financial Hygiene – It’s Good for You!

You went into business because you had a great idea, not because you love accounting. Bookkeeping chores, reading emails, and other administrative tasks may feel like nothing but distractions from reaching your goals. But staying on top of them is the best way to control the risks you run in business!

Gary Smith launched the eCommerce business Artesian City Marketing in the early 2000s, creating member stores and online employee uniform programs for companies like Bonnie Plant Farms.

After selling this business, he became an operations manager at an eCommerce web development agency. He currently works as a Strategic Partner Development Manager at Hostdedi, working with digital agencies to help make their relationship with Hostdedi a success.